Are you about to sell your property with seller-financing?

Do you want to make sure you get the maximum value for the real estate note you will create? Then pay close attention as we go over the five things you must do to create a valuable note.

1.) Bigger is Better (Cash Down Payment)

The amount and nature of a borrower’s down payment is critical to a real estate note’s value. While notes with little or no down payment can still be sold, the following guidelines help maximize value:

Cash Down Payment Guidelines

| Percentage of Sales Price | Quality |

|---|---|

| 10% or less | Poor |

| 10 – 15% | Fair |

| 15 – 20% | Good |

| 21% or greater | Great |

Note: Down payments made through repair credits or upgrades are less valuable than actual cash down payments.

Tip: Tax season is often the best time to secure a cash down payment, as borrowers may receive large IRS refunds.

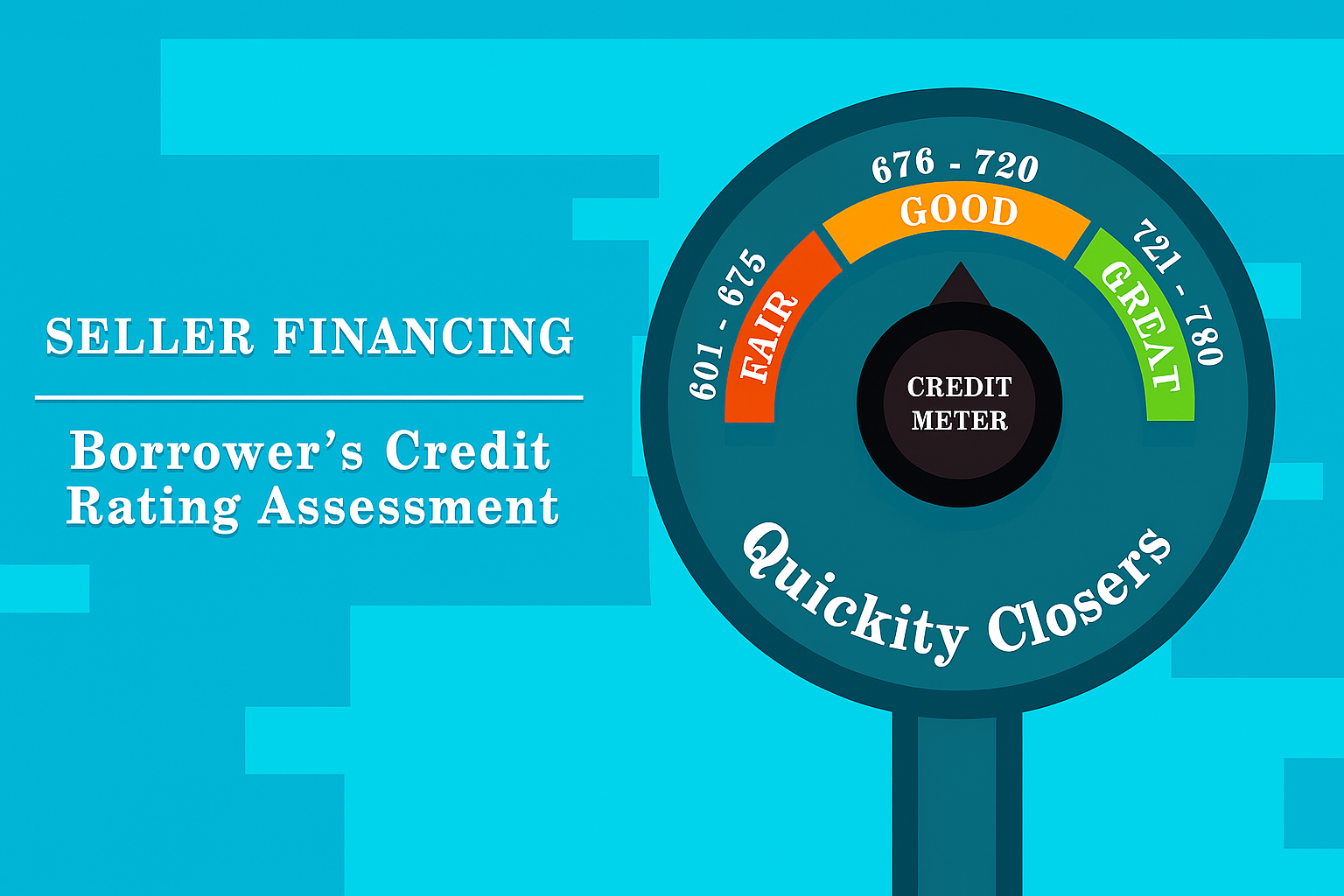

2.) Credit Scores

A borrower’s credit score is another key factor in determining note value. The middle score from Equifax, TransUnion, and Experian is typically used.

Borrower’s Credit Score Guidelines

| Credit Score | Quality |

|---|---|

| 600 or lower | Poor |

| 601 to 675 | Fair |

| 676 to 720 | Good |

| 720 or higher | Great |

3.) Interest Please (Interest Rates)

Notes with 0% interest or adjustable rates are less valuable due to risks like payment shock. Adjustable rate mortgages were a contributing factor to the 2007 subprime crisis.

To maximize value, notes should carry interest rates between 9% and 13%, or 3% to 7% higher than bank rates. Lower-risk borrowers may qualify for rates on the lower end of this range.

4.) Keep it Full (Fully Amortizing Loans)

Fully amortizing loans—those with equal payments throughout—are preferred. Partially amortized loans with balloon payments are riskier and less valuable.

5.) Length of Loan Guidelines

| Length of Loan | Quality |

|---|---|

| 11 years or longer | Poor |

| 8 to 10 years | Fair |

| 5 to 7 years | Great |

While longer-term notes (15, 20, or even 30 years) can still be sold, they are less valuable. In such cases, selling a partial note may be more beneficial.

6.) A Little Seasoning Please (Loan Seasoning)

Seasoning refers to how long a note has been held. It helps assess borrower payment consistency.

Seasoning Guidelines

| Months of Seasoning | Quality |

|---|---|

| 0 months | Unacceptable |

| 1 to 2 months | Poor |

| 3 to 5 months | Fair |

| 6 to 11 months | Good |

| 12 months or more | Great |

Notes with at least 1 month of seasoning and solid equity can still be sold.

7.) Keep Those Records (Record Keeping)

Proper documentation is essential:

- Store the original promissory note in a fire-resistant safe and keep a copy elsewhere.

- Retain the security instrument and closing documents (optional but helpful).

- Track all borrower payments, including the initial down payment.

- Avoid accepting cash; use checks or money orders and keep copies.

Final Thoughts

There are many factors that affect the value of a real estate note. Working with a knowledgeable attorney is highly recommended. Quickity Closers can purchase most notes—even those that don’t meet these guidelines—but following them helps avoid delays and ensures better pricing.

For a free, no-hassle Note Quote, call Quickity Closers at 1-855-724-2511.

Leave a Reply